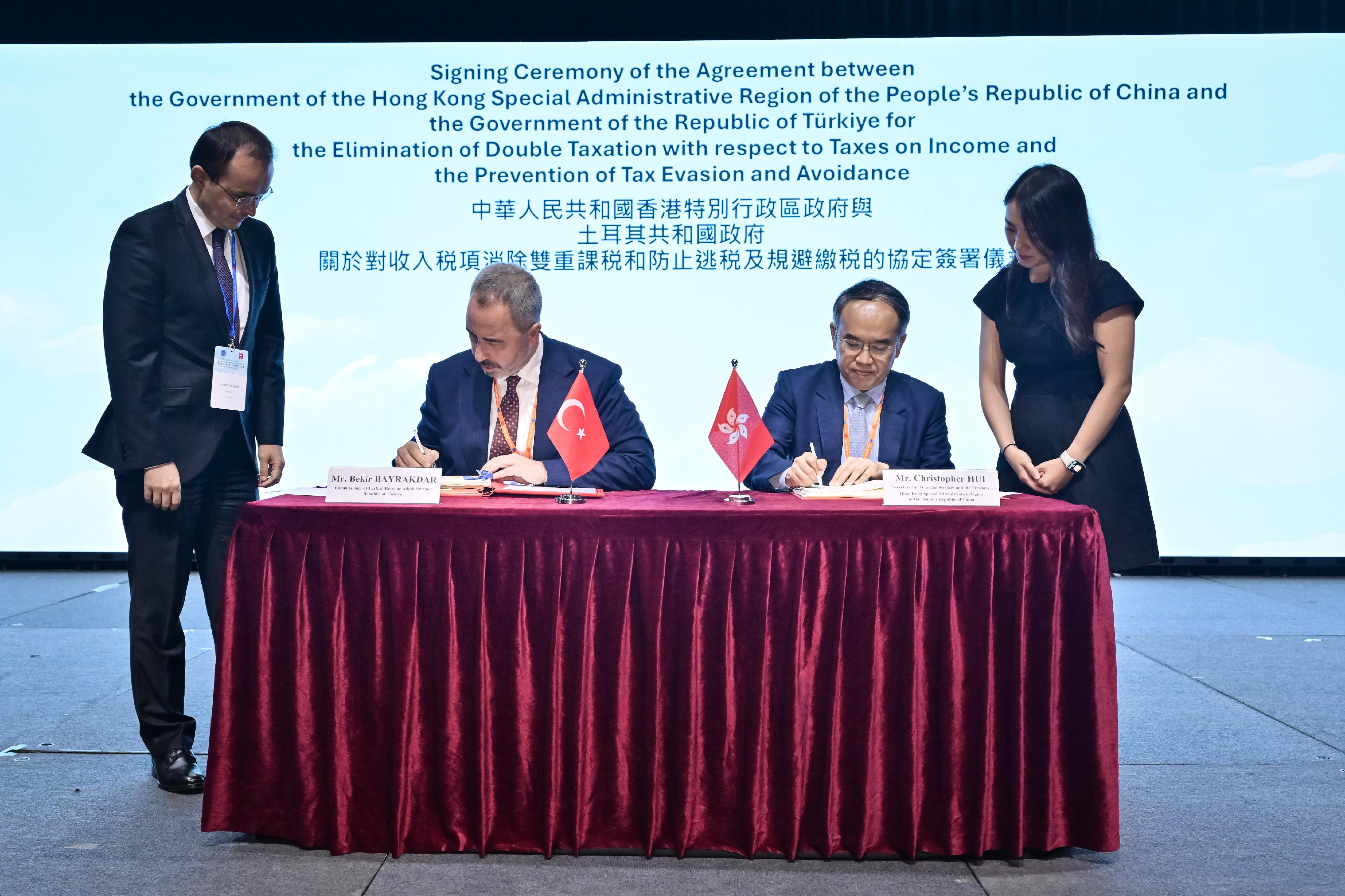

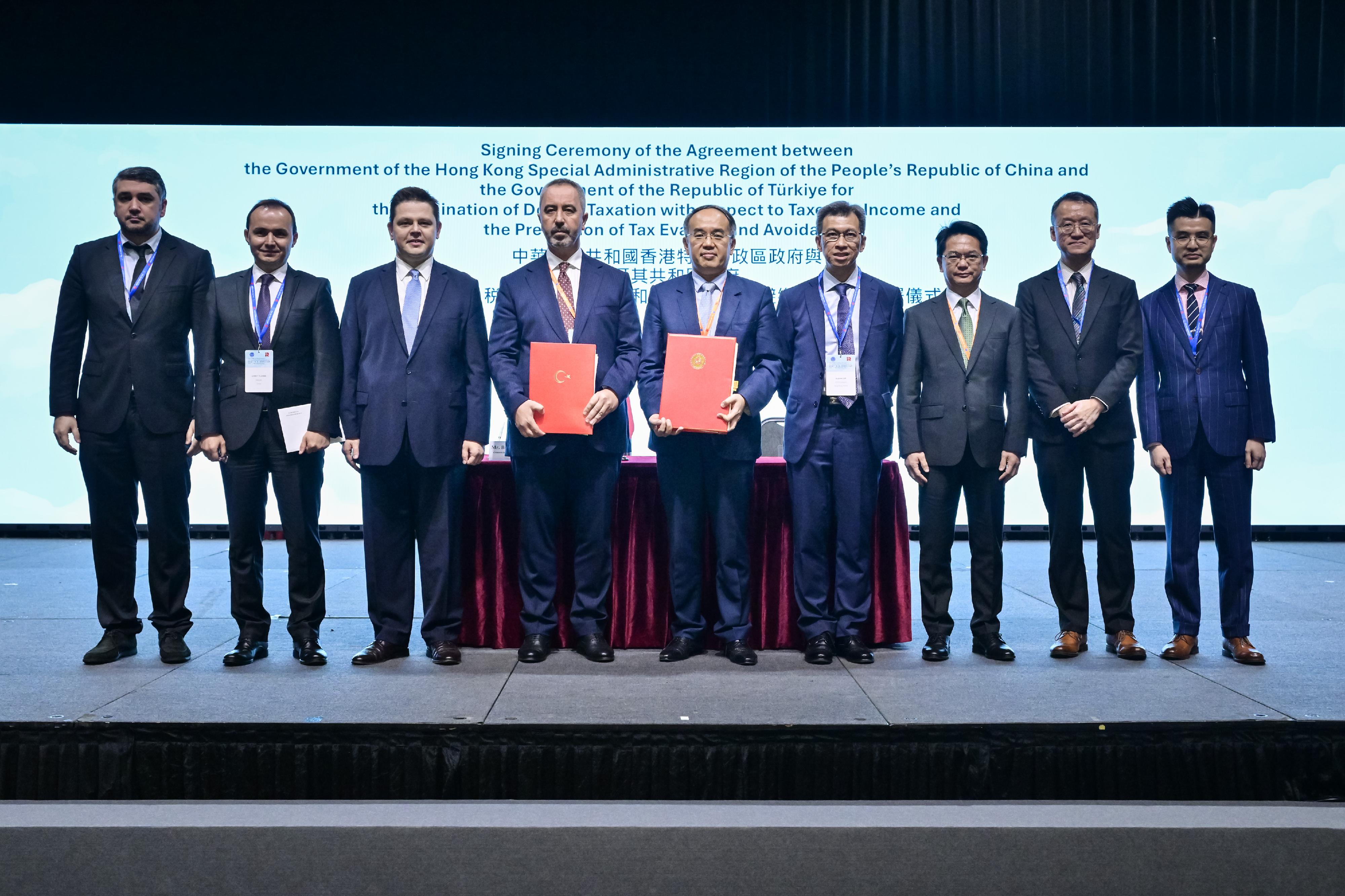

Hong Kong and Türkiye enter into tax pact (with photos)

*******************************************************

This CDTA is the 51st agreement that Hong Kong has concluded. It sets out the allocation of taxing rights between the two jurisdictions and will help investors better assess their potential tax liabilities from cross-border economic activities.

Mr Hui said, "Türkiye is participating in the Belt and Road Initiative. The signing of the CDTA between Hong Kong and Türkiye at the Fifth Belt and Road Initiative Tax Administration Cooperation Forum highlights the commitment of the two jurisdictions to deepening tax co-operation under the Belt and Road Initiative. I have every confidence that this CDTA will further promote economic and trade relations between Hong Kong and Türkiye, and contribute to the high-quality development of the Belt and Road Initiative through enhanced connectivity.

"We will continue to negotiate with trading and investment partners with a view to expanding Hong Kong's CDTA network. This will enhance the attractiveness of Hong Kong as a business and investment hub, and consolidate the city's status as an international economic and trade centre."

In accordance with the Hong Kong-Türkiye CDTA, Hong Kong companies can enjoy double taxation relief in that any tax paid in Türkiye, whether directly or by deduction, will be allowed as a credit against the tax payable in Hong Kong in respect of the same income, subject to the provisions of the tax laws of Hong Kong.

Moreover, the Hong Kong-Türkiye CDTA also provides the following tax relief arrangements:

(a) Türkiye's withholding tax rate for Hong Kong residents on dividends will be capped at 5 per cent or 10 per cent (depending on the percentage of their shareholdings); while that on interest and royalties will be capped at 10 per cent, and further reduced to 7.5 per cent if the interest is received by a financial institution in respect of a loan or debt instrument with a maturity period exceeding two years, or if the royalties are for the use of, or the right to use, industrial, commercial or scientific equipment;

(b) Hong Kong airlines operating flights to and from Hong Kong and Türkiye will be taxed at Hong Kong's corporation tax rate on their profits, and will not be taxed in Türkiye; and

(c) Profits from international shipping transport earned by Hong Kong residents arising in Türkiye will not be taxed in Türkiye.

The CDTA will come into force after the completion of ratification procedures by both jurisdictions. In Hong Kong, the Chief Executive in Council will make an order under the Inland Revenue Ordinance (Cap. 112), which is subject to negative vetting by the Legislative Council.

Details of the Hong Kong-Türkiye CDTA can be found on the Inland Revenue Department's website (www.ird.gov.hk/eng/pdf/Agreement_Turkiye_HongKong.pdf).

Ends/Tuesday, September 24, 2024

Issued at HKT 20:15

Issued at HKT 20:15

NNNN

Photo

Related Links

Speech by CE at 5th Belt and Road Initiative Tax Administration Cooperation Forum (English only) (with photos/video)

5th Belt and Road Initiative Tax Administration Cooperation Forum opens today to deepen international tax co-operation in pursuit of high-quality Belt and Road development (with photos)

SFST's speech at 5th Belt and Road Initiative Tax Administration Cooperation Forum welcome dinner (English only) (with photo)

5th Belt and Road Initiative Tax Administration Cooperation Forum concludes successfully (with photos)